Key regulatory developments in 2019

Proskauer’s 2019 Annual Review listed updates on UK tax, the relationship between the UK and the EU, as well as cyber security and privacy law.

UK tax

There are two areas of development in relation to the international focus on tackling tax avoidance and increasing transparency of tax arrangements.

Hybrid mismatches

The UK responded to the OECD’s recommendation on Action 2, which was about neutralising effects of hybrid mismatch arrangements, and legislation was brought in under the Finance Act 2016.

Profile:

Categories: NewsFundraising & fund structuringRegs & ComplianceTaxTechnologyCyber security

More from The Drawdown

17 April 2024

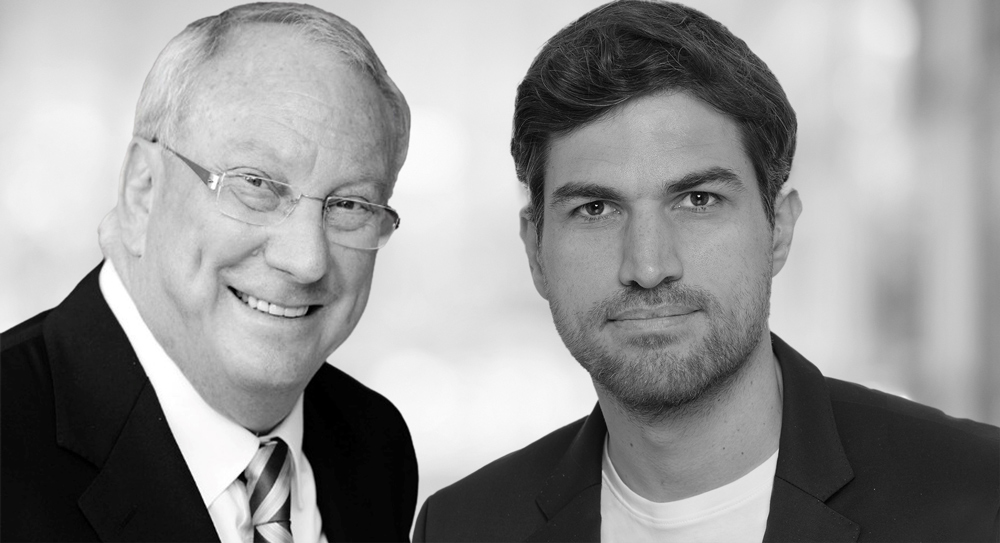

Carlyle appoints tax leadership

The firm’s own Clare Copeland (left) takes up the mantle of chief tax officer as Shannon Stafford (right) is appointed chair of tax

16 April 2024

Chronograph launches Chrono AI

The tool will assists LPs with portfolio monitoring and analysis

16 April 2024

Ark launches automated fund accounting solution

The cloud-based technology supports fund administrators and GPs with fund operations and investor relations

16 April 2024

NLC appoints non-exec director and CTO

Investec co-founder Bernard Kantor and ex-Meta Kresimir Slugan join the independent non-bank lender, respectively

16 April 2024

WTW launches PE LTAF

Insurance company’s DC pension schemes trust among allocators; initial commitments before launch sit at £450m

15 April 2024

EFRAG approves double-materiality guidelines

ESRS FAQ has been updated to explain when mitigating actions are considered, among other updates